[ad_1]

Oil and gas industries just appreciated a bumper earnings calendar year, with shareholders seeing report payouts. In its wake, Europe’s Shell and BP the two walked back again on their ambitious small-carbon transition programs, with corporations across the sector expanding their investing in new creation.

That’s not superior information for local weather alter, mostly driven by burning fossil fuels. One stress is these investments imply the business and its political allies will struggle tooth and nail for them to steer clear of “stranded property” losses, locking in greater output of local climate changing fuels for yrs and even many years to occur.

Not only the businesses, but also their shareholders could transform, as vested interests, into a wide coalition versus eco-friendly vitality. At the very least in the U.S. and the U.K., most pensions are invested in cash marketplaces, where by inside inventory markets oil and fuel organizations stay amid the most reputable generators of dividends and share buybacks. All of this could discourage governments from applying all-also-formidable local climate mitigation policies for panic of producing economic losses to a wide swath of their personal voters.

But centered on a new analysis, we argue that higher-income governments will need not stress about triggering these financial losses. That is mainly because most hits from stranded fossil fuel assets—lower output volumes or gross sales at reduced price ranges than traders expected—would tumble principally on the rich associates of these countries. That ain’t most voters.

The rationalization is fairly straightforward: these nations all have important inequality in who owns firms. That signifies the rich usually very own the vast vast majority of all shares and bonds, and there is no evidence that differs appreciably in the oil and fuel sector.

Governments should really without a doubt be concerned about opportunity results on the customers of fossil fuels, amongst motor vehicle homeowners for illustration, brought on by carbon prices and other weather guidelines that impose penalties on consumption, and there have been important proposals for actions to decrease the adverse results of fossil gasoline phaseout on the most susceptible folks in culture, this sort of as “carbon dividends” and enhanced community transport. Governments should really also worry about personnel in the power and other sectors and assure a just transition for fossil fuel communities. Nevertheless, for monetary investments, the base 50 per cent and even 90 per cent of prosperity owners could be compensated at really minor value as opposed to these other steps.

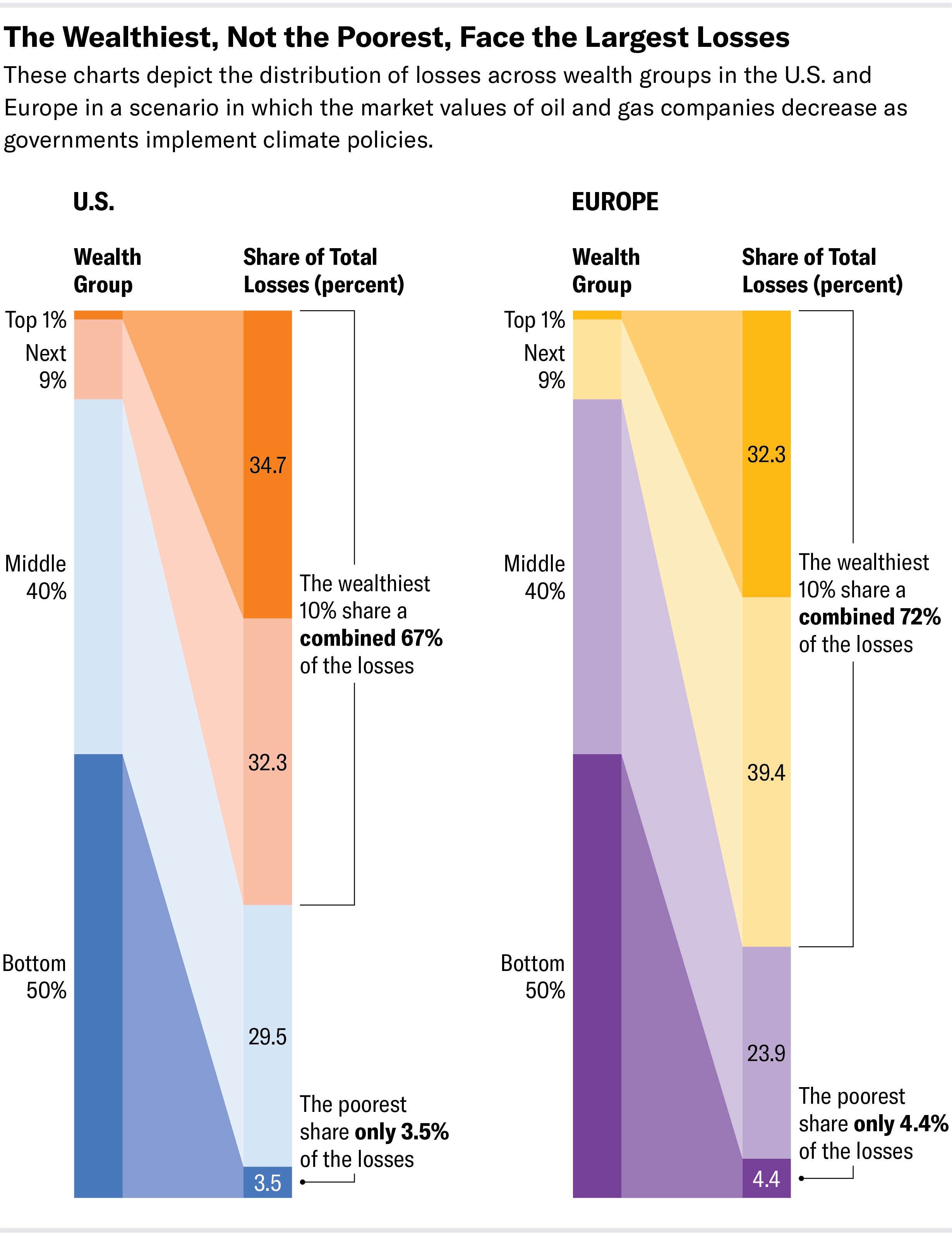

We have beforehand calculated that in a scenario in which oil and fuel businesses are originally valued centered on an expectation of participation in a expanding oil and gasoline industry, but governments about the world put into practice climate insurance policies restricting worldwide warming to 2 levels Celsius over preindustrial averages, this could guide to prosperity losses of virtually $550 billion for U.S. and European shareholders as companies’ current market values are readjusted to these decrease anticipations. On the other hand, as soon as we review where by these shareholders are possible to sit in the prosperity distribution, it turns out that only 3.5 % in the U.S. and 4.4 per cent in Europe of the losses damage the portfolios of the base 50 per cent of them (see chart). Basically place, individuals who own most shares, also own most of the oil and fuel sector shares that get devalued.

Since the top rated 1 % and major 10 percent are so wealthy on the other hand (each individual U.S. American adult in the best 1 % owns more than $13 million in net prosperity on normal) these losses, distribute across men and women, rarely display in their portfolio. We estimate that losses quantity to less than 50 % a p.c of the web prosperity of wealthiest 1 per cent or 10 p.c of People, for instance. Also, as fossil fuels decrease, new expenditure options arise in the developing marketplaces for lower-carbon choices that allow for for portfolio hedging. Even losses for the the very least rich 50 percent and 90 % are not large as a percentage of their wealth. The issue could crop up from the simple fact that they have so minimal prosperity in the initial location. Compensating the bottom 50 per cent would cost just $12 billion in the U.S. and $9 billion in Europe in a $550 billion decline situation. This could be paid off with just one particular sixth of the annual revenue from a notional $13 for each ton of carbon dioxide emissions selling price in the U.S., which is substantially lower than latest consensus estimates of the social charge of carbon. In Europe, it could also be paid out off with about 20 percent of the earnings from the European Emissions Buying and selling Technique (ETS) in 2022.

One could argue that the rich are significantly extra advanced investors and will get out of their investments right before the shares drop their value, saddling the inadequate with significantly more of the losses. This is without a doubt a problem, however our robustness calculations recommend that even if the poor were being considerably more probably to very own oil and gasoline shares, compensation costs would continue to be limited.

There are several obstacles to moving absent from fossil fuels, from prices for customers and companies to employment and which means in communities where by fossil fuel manufacturing is concentrated. Governments have to tackle them all cautiously. Even so, losses for fiscal traders do not rank among them, and even if they have been, we clearly show that compensation for any socially pertinent losses would be low-priced in fact.

Warnings about pension losses and pushback versus measures that would trigger asset stranding show up largely designed in the fascination of the quite rich, whose potential to absorb losses is arguably much larger than everybody else’s. Losses from unmitigated local weather modify, on the other hand, will possible hit the poor and susceptible considerably more durable.

This is an opinion and assessment posting, and the views expressed by the author or authors are not essentially those people of Scientific American.

[ad_2]

Resource backlink